When Simple Beats Sophisticated

7 min read

7 min read

When Simple Beats Sophisticated

The Puzzle of Simplicity

How does TiltFolio Balanced, a simple buy-and-hold portfolio of bonds, stocks, and gold, stack up against funds operated by the world’s biggest and most sophisticated money managers?

At first glance, the comparison seems almost absurd. Bridgewater Associates, the world’s largest hedge fund, manages more than $100 billion and employs hundreds of highly trained professionals. Their flagship “All Weather” strategy was designed in the 1990s to handle virtually any economic environment. Other firms like AQR and Man AHL run competing versions of the same concept, marketed under the umbrella term risk parity.

And yet, as surprising as it may sound, TiltFolio Balanced (an allocation that almost anyone can implement in a brokerage account) has quietly outperformed many of these heavyweight strategies.

The lesson? In long-term investing, simplicity often beats complexity.

The Origins of Risk Parity

The idea behind Bridgewater’s All Weather Fund was both elegant and practical. Instead of constantly trying (and usually failing) to predict the next market move, construct a portfolio of uncorrelated assets that balances risk across different environments.

The insight was that portfolio weights should not simply reflect capital allocations but risk contributions. Bonds, for example, are far less volatile than stocks or gold, so they receive a higher allocation to equalize their impact. That’s why TiltFolio Balanced allocates roughly half of its weight to government bonds, not out of optimism for bonds’ long-term returns, but because they act as stabilizers when stocks or gold are swinging.

Bridgewater was famously secretive about the precise recipe, but over time enough information leaked out to allow investors and academics to approximate All Weather’s design. The core idea (risk-balanced diversification) became the foundation for an entire category of institutional strategies.

Risk Parity’s Recent Stumbles

Despite decades of success, Bridgewater’s All Weather Fund and its peers have struggled in recent years. A Bloomberg article highlighted disappointing performance across the risk parity universe, raising questions about whether the approach still works.

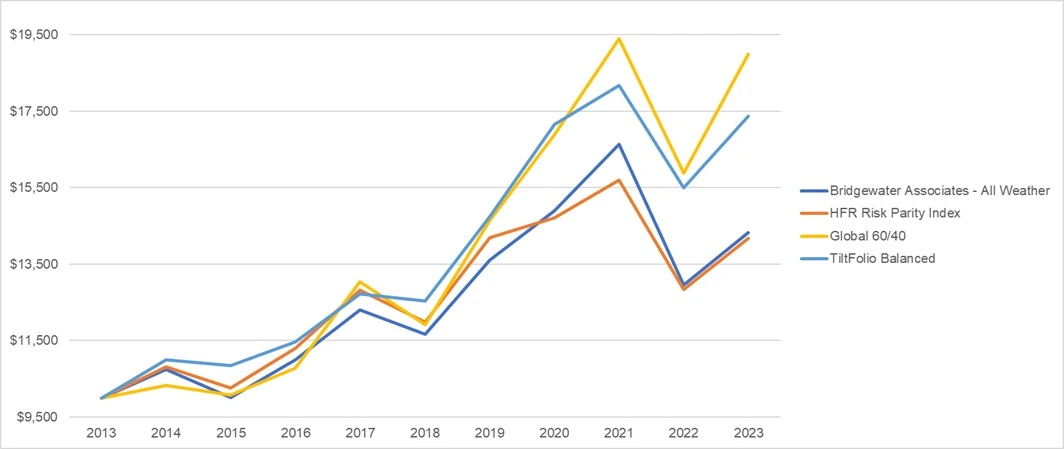

Before writing off an entire philosophy, though, it’s worth digging into the numbers. To get a clearer picture, let’s compare four strategies over the decade from 2014 to 2023:

• HFR Risk Parity Index (10% volatility target)

• TiltFolio Balanced

• Global 60/40 portfolio (stocks and bonds only)

Here’s what $10,000 invested in each would have grown to after 10 years:

• HFR Risk Parity Index: $14,176 (3.6%/year)

• TiltFolio Balanced: $17,378 (5.7%/year)

• Global 60/40: $18,995 (6.6%/year)

These results are striking. Even without using leverage (a built-in advantage for institutional risk parity funds), TiltFolio Balanced came out comfortably ahead.

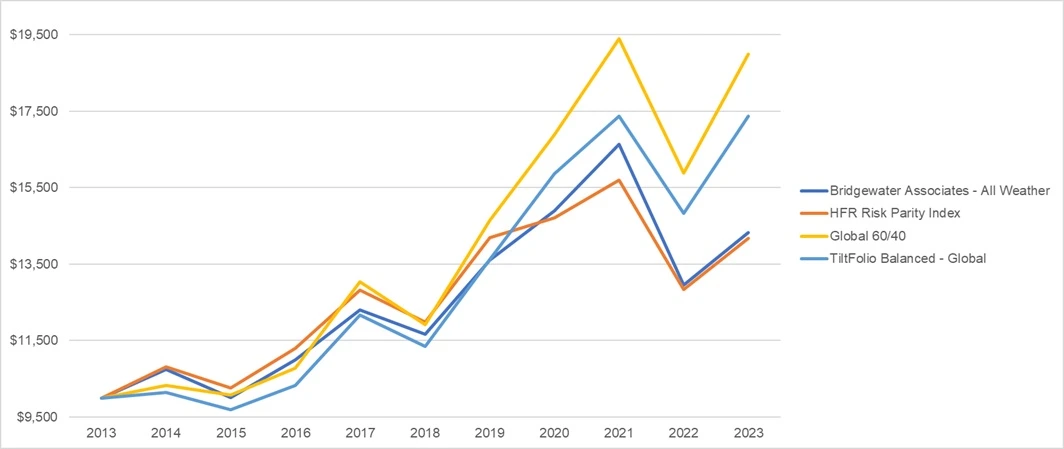

Addressing the “U.S. Bias”

Skeptics might argue that TiltFolio Balanced benefited unfairly from U.S. outperformance. After all, U.S. stocks and the dollar led the world during this period. To test this, we rebuilt TiltFolio Balanced using global stocks (MSCI ACWI) and global bonds (Bloomberg Global Aggregate) instead of their U.S.-only counterparts.

The result? Virtually identical. Over the same 10-year window, the global version of TiltFolio Balanced delivered nearly the same return profile, still ahead of the institutional risk parity benchmarks.

Breaking Down Asset Performance

Looking under the hood, here’s how the individual components performed between 2014 and 2023:

• Global bonds (Bloomberg Aggregate): $14,888 (4.1%/year)

• Gold: $16,827 (5.3%/year)

The challenge for risk parity strategies becomes obvious: this was a decade dominated by equities. Any portfolio that spreads risk across multiple asset classes will lag during such an environment. TiltFolio Balanced and risk parity peers alike trailed the global 60/40 benchmark for this reason.

But this is by design. Risk parity strategies aren’t meant to beat stocks in a stock bull market; they’re meant to protect capital and compound steadily across environments.

Why Risk Parity Still Matters

So does the underperformance of All Weather and other risk parity funds mean the idea is broken? Hardly.

Consider two points:

2. TiltFolio Balanced still won on simplicity. Despite lacking leverage, complex models, or armies of analysts, it outperformed the institutional risk parity benchmarks.

The conclusion isn’t that risk parity is dead. It’s that most investors overcomplicate it. By the time you factor in high fees, layers of derivatives, and the temptation to “improve” the formula, the net result often falls short of what a simple implementation can achieve.

Why TiltFolio Balanced Works

TiltFolio Balanced isn’t magic. It’s simply the cleanest expression of the risk parity philosophy. A 50/30/20 mix of bonds, stocks, and gold smooths out volatility, reduces drawdowns, and ensures that no single asset class dominates returns.

More importantly, it strips away unnecessary complexity. Investors don’t need leverage, exotic instruments, or opaque models. They just need discipline and a willingness to stick with a balanced approach through cycles.

Over more than 50 years of backtested history, TiltFolio Balanced has shown:

• A maximum drawdown of approximately 20%, far less than equity markets

• Returns that, while modest compared to pure stocks, are much smoother and easier to live with

The Real Lesson

The real story here isn’t about Bridgewater or TiltFolio. It’s about the broader lesson that simplicity often outperforms sophistication in investing.

When you strip away fees, leverage, and complexity, what’s left is the timeless power of diversification. That’s the foundation of TiltFolio Balanced, and why it continues to shine, even against the world’s largest and most sophisticated funds.

Final Thoughts

Criticism of Bridgewater’s All Weather Fund may be fashionable, but it misses the bigger point. Risk parity remains a sound idea, one that has stood the test of decades. The problem isn’t the philosophy; it’s the execution.

TiltFolio Balanced demonstrates that a radically simple, transparent implementation can deliver better results than billion-dollar hedge funds with armies of analysts. For individuals and institutions alike, it is an excellent starting point: reliable, resilient, and refreshingly easy to understand.

In investing, as in life, sometimes the simplest solution is the best one.

How TiltFolio Works Series

This post is part of the “How TiltFolio Works” series. Explore all posts in the series:

- TiltFolio Explained: A Smarter Alternative to 60/40 Portfolios

- Explaining TiltFolio Through Car Brands

- Why the Modern World Needs TiltFolio

- Why TiltFolio Balanced Is the Foundation

- The Ancient Origins of Portfolio Diversification

- TiltFolio Balanced as a Market Barometer

- When Simple Beats Sophisticated

- Decades of Perspective: What TiltFolio Balanced Teaches Us About the Future

- Building a Simple Trend-Following System

- Beyond Moving Averages: Why Volatility Trends Matter More Than You Think

- How TiltFolio Adaptive Differs From Traditional Trend-Following

- Will Trend-Following Keep Working?

- When Trend-Following Underperforms

- How to Avoid Curve-Fitting in Trend-Following

- The “Secret” to the Best Risk-Adjusted Returns: Correlations

- From Rollercoaster to Escalator: Finding Your Investing A-ha Moment

- TiltFolio’s Main Edge: Reliability That Compounds

- How to Stay Committed to an Investment Plan