TiltFolio Explained: A Smarter Alternative to 60/40 Portfolios

7 min read

7 min read

TiltFolio Explained: A Smarter Alternative to 60/40 Portfolios

One of the most consistent pieces of feedback I hear from new TiltFolio readers is: “Your posts are like a foreign language.”

I get it. Concepts like “asset allocation,” “trend following,” and “volatility” don’t exactly make for light reading. And truthfully, TiltFolio was designed for investors who already have some experience with advanced investing ideas.

But investing doesn’t have to be intimidating. The problems TiltFolio tries to solve can be explained step-by-step. In this post, I’ll break down exactly what TiltFolio is, why it exists, and how it improves on the portfolios most people are told to follow.

The Problem with Today’s Money

Let’s start at the root of the problem: our money.

We live in a fiat money system, meaning currencies like the dollar, euro, and pound are not tied to anything tangible like gold. Instead, they’re backed by government decree and central bank policy.

This system comes with a chronic side effect: inflation. Even when inflation is “only” 3% per year, prices rise by about 34% over a decade. That means the same basket of groceries, the same car, or the same home costs a third more in just ten years. Meanwhile your cash savings lose purchasing power just sitting in the bank.

This wasn’t always the case. For centuries, when either gold or silver served as money, inflation was rare outside of major wars. A remarkable study of England’s economic history showed almost no inflation over 700 years, until the world abandoned gold in the 20th century. After World War I, when nations dropped the gold standard, inflation took off. It accelerated again in the 1970s, after U.S. President Nixon cut the final tie between the dollar and gold.

Inflation isn’t just a background annoyance. It’s one of the biggest threats to long-term wealth. And yet, most traditional investment advice barely addresses it.

The Problem with Today’s Portfolios

If inflation eats away at savings, then the obvious solution is investing. But here too, the advice most people get is flawed.

For decades, financial advisors and robo-advisors have pushed versions of the “60/40 portfolio”: 60% stocks, 40% bonds - rebalanced annually. It’s often described as “moderate risk.”

In reality, this portfolio is dominated by stocks. If stocks perform well, so does the portfolio. If stocks perform poorly, so does the portfolio. Bonds may cushion the blow a little, but not enough. And during periods of high inflation, neither stocks nor bonds provide protection.

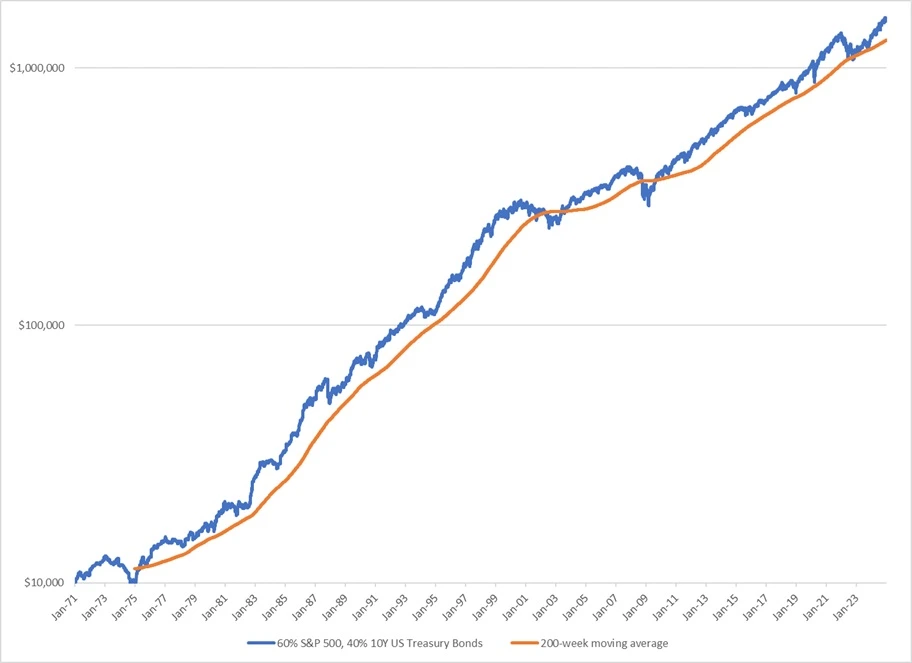

A look at the data proves the point. Since 1971, when the gold standard was abandoned:

60/40 Portfolio Performance

• Annualized volatility: 10.4%

• Maximum drawdown: –29.7%

That looks good on paper, but the reality is rougher. The equity curve for 60/40 often sinks back toward its long-term trendline. There are plenty of -20% drawdowns over the years.

Simply put, this portfolio is far too volatile for anyone who needs reliable returns, such as retirees.

A Smarter Foundation: TiltFolio Balanced

TiltFolio’s first step was simple: fix the flaws of 60/40.

The fix has two parts:

• Adjust portfolio weights so that stocks, bonds, and gold each contribute equally to risk and returns, rather than letting stocks dominate.

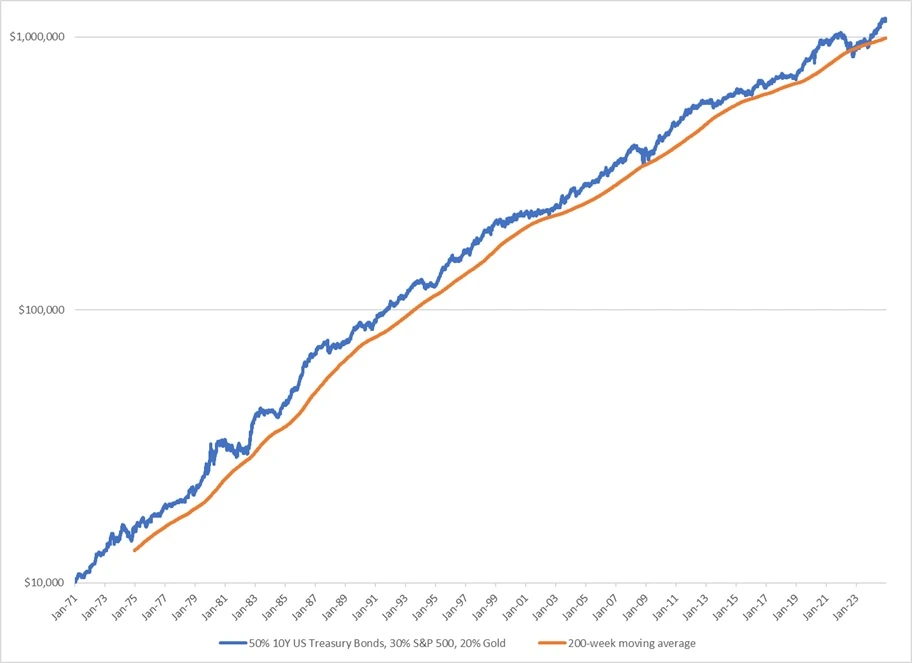

The result is what we call TiltFolio Balanced: 50% bonds, 30% stocks, 20% gold - rebalanced annually.

The numbers speak for themselves:

TiltFolio Balanced Performance

• Annualized volatility: 7.4%

• Maximum drawdown: –18.2%

This is a significant improvement: similar returns, but with much less risk. The equity curve is far smoother, rarely dipping below its long-term trendline. Losses are rarer and shallower, and the portfolio has never lost money two years in a row.

If this looks familiar, it should. This portfolio is a simplified version of Bridgewater Associates’ legendary All Weather strategy. Ray Dalio and his team pioneered the idea that portfolios should be balanced across economic environments, not just dominated by one asset class.

For investors who want the smoothest possible ride with predictable risks, this is an excellent starting point.

TiltFolio Adaptive: The Next Step

But what if we could go further?

TiltFolio Balanced is a “buy-and-hold” strategy. It doesn’t adapt. It just sits there, waiting. That makes it reliable, but limited.

TiltFolio Adaptive takes the next step: systematically tilting toward the asset class most likely to outperform in the future.

The logic is simple: markets move in trends. Asset classes that are strong tend to stay strong for a time, while weak ones tend to stay weak. By tracking volatility trends, TiltFolio Adaptive can determine when to take risk (“risk-on”) and when to pull back (“risk-off”). Within those regimes, it tilts fully into whichever asset class: stocks, bonds, gold, or commodities is in the strongest positive trend.

This approach gives investors two things:

• The ability to capture outsized returns during strong uptrends.

It’s not magic, and it doesn’t win every trade. But over the long run, it systematically puts the odds in your favor.

So, What is TiltFolio?

At its core, TiltFolio is a response to two frustrations:

• Buy-and-hold portfolios don't adapt to changing market conditions.

The first step was building a smarter benchmark: TiltFolio Balanced. The second step was adding a systematic trend-following overlay to tilt toward the best-performing asset class: TiltFolio Adaptive.

The result is TiltFolio: two complementary portfolio strategies designed to protect wealth from inflation, smooth returns, and capture growth when opportunities arise.

For some, that may sound technical. But the philosophy is simple:

• Don't bet everything on one asset class long-term.

• Don't sit still when markets move.

That’s TiltFolio in plain English: TiltFolio Balanced for steady, diversified growth, and TiltFolio Adaptive for dynamic, trend-following returns.

How TiltFolio Works Series

This post is part of the “How TiltFolio Works” series. Explore all posts in the series:

- TiltFolio Explained: A Smarter Alternative to 60/40 Portfolios

- Explaining TiltFolio Through Car Brands

- Why the Modern World Needs TiltFolio

- Why TiltFolio Balanced Is the Foundation

- The Ancient Origins of Portfolio Diversification

- TiltFolio Balanced as a Market Barometer

- When Simple Beats Sophisticated

- Decades of Perspective: What TiltFolio Balanced Teaches Us About the Future

- Building a Simple Trend-Following System

- Beyond Moving Averages: Why Volatility Trends Matter More Than You Think

- How TiltFolio Adaptive Differs From Traditional Trend-Following

- Will Trend-Following Keep Working?

- When Trend-Following Underperforms

- How to Avoid Curve-Fitting in Trend-Following

- The “Secret” to the Best Risk-Adjusted Returns: Correlations

- From Rollercoaster to Escalator: Finding Your Investing A-ha Moment

- TiltFolio’s Main Edge: Reliability That Compounds

- How to Stay Committed to an Investment Plan