Gold's Role as a Monetary Anchor

7 min read

7 min read

Gold’s Role as a Monetary Anchor

Money is one of the earliest inventions of civilization. Without it, trade collapses into a chaotic system of barter. Imagine a society with 1,000 different goods. To exchange them without a common yardstick, you’d need 499,500 different prices, each expressed in terms of another good. A bag of grain might cost three chickens. A fishing net might cost half a goat. And so on. As the number of goods and services expands, this system becomes unmanageable.

Money solved this problem. By choosing a common standard of value, societies gained the ability to price goods consistently, store wealth, and transact across time and distance. The question was: what should that standard be?

The Long Search for Money

History is full of experiments. In ancient Rome, salt was so valuable that it served as currency (the origin of the word salary). Other societies tried seashells, spices, silver, even giant rocks imported from distant islands. In modern times, cigarettes became money in prisons, while Levi’s jeans functioned as currency in the former USSR.

Through trial and error, however, nearly every major economy converged on gold. The turning point came in 1717, when Sir Isaac Newton, then Master of the Royal Mint, set the price of gold in England and ushered in the modern gold standard. Before that, England used a bimetallic system (silver for smaller coins, gold for larger ones). But Newton’s decision tilted the balance decisively toward gold, and over time, the rest of the world followed.

China was the notable exception, experimenting with paper money as early as the 11th century. But elsewhere, gold’s universal appeal (scarce, durable, divisible, and easily recognizable) made it the ultimate anchor for money.

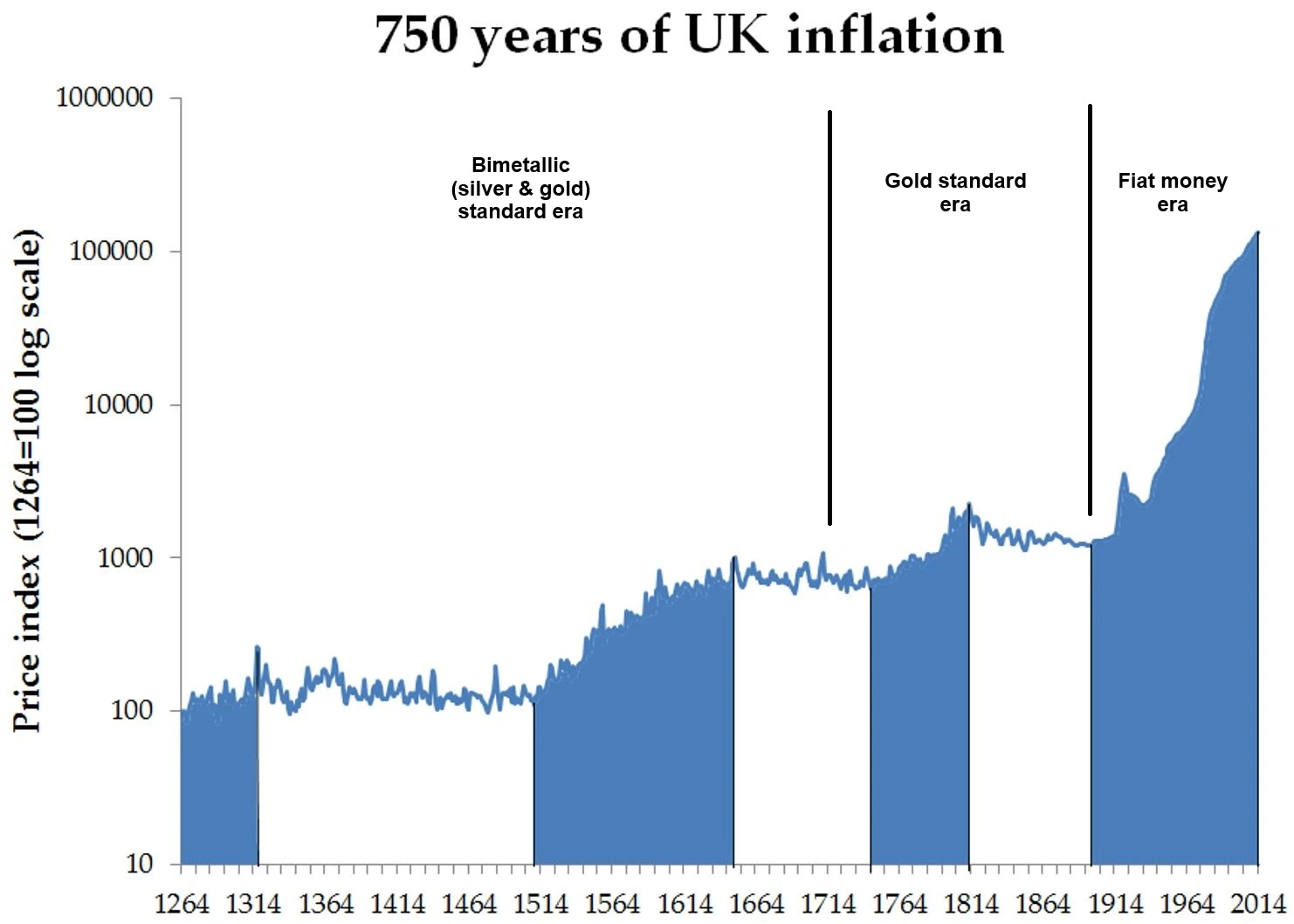

A 700-Year Experiment in Price Stability

A recent study of English prices across seven centuries reveals something remarkable. Under both the silver-gold bimetallic standard and later the pure gold standard, inflation was virtually nonexistent.

In 1717, when Newton set the gold standard, England’s wholesale price index stood at a level it had maintained for over a hundred years. By 1930, after two centuries marked by industrial revolutions, global wars, and massive political upheavals, that same index was… still about where it started. Prices that would have tripled, quadrupled, or worse under today’s fiat system barely budged.

This chart dramatically illustrates the price stability achieved under the gold and bimetallic standards, showing how prices remained remarkably stable for over centuries despite major historical events.

In other words, while the world transformed beyond recognition, gold kept money (and therefore daily life) anchored in stability.

The Modern Inflation Puzzle

Contrast that with today. Inflation, and its twin danger deflation, dominate economic debate. After the COVID-19 pandemic, some blamed excessive government spending for price surges. Others pointed to central banks, particularly the Federal Reserve, for acting too slowly to raise interest rates. Entire new asset classes, like cryptocurrencies, have emerged claiming to solve the problem of inflation once and for all.

And yet, history suggests the solution isn’t complicated at all. The simplest way to tame inflation is to tie money creation to a stable unit of account: gold.

How the Gold Standard Worked

Under a gold standard, managing “monetary policy” was refreshingly straightforward.

English economist Stanley Jevons described the mechanism in his book Money and the Mechanism of Exchange published in 1903.

• If gold traded below its target price (say, more than 1% lower), the central bank would inject money. It could print currency to buy gold or government bonds, putting cash back into the economy.

That was it. No 500-strong research team at the Federal Reserve. No armies of central bankers debating abstract models. Just a simple, rules-based mechanism that kept the money supply tethered to a real anchor.

The system worked precisely because it removed human discretion. Gold provided discipline. Politicians and central bankers couldn’t inflate their way out of debt or juice the economy before an election. Money creation was constrained by the anchor.

Gold as a Yardstick, Not a Commodity

One of the great misunderstandings about gold is that it is valuable because it is a timeless store of wealth. In reality, gold’s power came from its role as a yardstick.

Think of it like a ruler. A ruler isn’t inherently valuable because it’s made of wood or plastic (it’s valuable because it provides a consistent measure of length). Gold worked the same way. By anchoring money to gold, societies could transact with confidence that the unit of account would remain stable.

Yes, large discoveries of gold could temporarily disrupt the system (think of Spain’s influx of New World gold in the 16th century). But outside of rare shocks, the gold standard didn’t allow persistent inflation or deflation.

Why Did We Abandon It?

If the gold standard was so effective, why did we leave it behind? The answer is politics.

Modern money has become a political instrument. Governments prefer the flexibility to print money when debts pile up or when voters demand more spending. Central banks prefer the freedom to manipulate interest rates and liquidity in pursuit of growth. In short, fiat money serves politicians and policymakers far better than it serves ordinary citizens.

Gold, by contrast, imposed discipline. And discipline rarely wins elections.

Gold’s New Role: Alarm Bell

While gold no longer serves as the world’s direct monetary anchor, it hasn’t disappeared from the system. Instead, gold now plays the role of an alarm bell.

Since 1971, when the U.S. officially abandoned the gold standard, gold has returned 8.8% per year. That’s based on gold trading at $38 per ounce at the outset of 1971 and above $3,600 in September 2025. That long-term climb isn’t because gold suddenly became more useful, but because it has reflected the steady debasement of fiat money. Whenever governments or central banks overreach, gold tends to surge (reminding us that monetary stability has been sacrificed for short-term expediency).

As Mark Twain wrote: “Customs are rock, laws are sand.” Fiat money may dominate today, but gold remains the rock that reveals the cracks in the system.

TiltFolio’s View on Gold

This is why gold plays a central role in TiltFolio’s strategies.

• TiltFolio Adaptive frequently rotates into gold when trend-following signals suggest accelerated currency debasement. In moments when fiat trust erodes quickly, gold often becomes the best-performing asset, and Adaptive ensures investors participate in those moves.

For us, gold is not a relic. It’s a core tool for building portfolios that are resilient to the uncertainties of modern money.

Conclusion: The Case for Anchors

The story of money is the story of civilization itself. Societies have always needed a stable yardstick to measure value, and through centuries of experimentation, gold proved itself as the most reliable anchor.

We may live in a fiat world today, but the lesson of history is clear: anchoring money to something real tames inflation, preserves trust, and stabilizes economies.

Gold may no longer sit at the center of the monetary system, but it remains the most important check on its excesses. And for investors, that makes it indispensable, not as a store of value, but as a portfolio anchor.

{kind=link}